Now that the government has directly intervened in exchange-rate defense, the risk of being designated a currency manipulator by the U.S Treasury looms

[Choice Times=Jinan Kim, Former Executive Director, Samsung Electronics Middle East ]

As the exchange rate crossed 1,485 won per dollar, the government resorted to extreme measures.

The foreign exchange authorities moved beyond verbal intervention and demonstrated action.

Immediately after the foreign exchange market opened, senior officials from the Ministry of Economy and Finance and the Bank of Korea stated, “Excessive weakness of the won is undesirable. You will soon see the government’s strong will and its comprehensive capacity to execute policy.” Even the presidential office’s chief policy secretary stepped forward, declaring, “From now on, we will respond with action, not words.”

Not long ago, the vice minister of economy and finance summoned executives of major conglomerates and pressured them to release the dollars they were holding. With dollar demand expected to surge next year due to the establishment of factories in the United States, the government was effectively urging companies to sell dollars immediately—almost a form of coercion.

From the perspective of profit-seeking firms, this demand is baffling: it amounts to selling dollars cheaply now only to repurchase them later at a higher price. In effect, it asks companies to sacrifice for the government. At a time when even existing dollar holdings are insufficient to cover planned investments and additional purchases are needed, it is unrealistic to expect such demands to work on large corporations.

In line with the government’s strong stance, the National Pension Service (NPS) has reportedly begun large-scale currency hedging in recent days. Even the nation’s retirement funds have been mobilized for exchange-rate defense. When the NPS conducts large-scale hedging using dollars obtained through currency swaps with the Bank of Korea, it helps suppress the weakening of the won.

However, if the exchange rate continues to rise, the NPS must absorb losses equivalent to the hedged amount. Had it done nothing, it would have benefited from the rising exchange rate.

On the 24th, the government also announced a measure exempting capital gains tax—up to 50 million won—if so-called “Seohak Ants” (Korean retail investors in U.S. stocks) switch their investments back to the domestic market. Normally, profits from U.S. stock investments are subject to a 22% capital gains tax when repatriated. Under the new measure, investors who switch to domestic stocks and hold them for one year would be exempt.

Frankly, it is doubtful whether this tax exemption will be effective. If the outlook for U.S. markets is better than the benefit gained from tax relief, there is no reason to move funds into the domestic market—especially with the condition that funds be locked up for a full year.

In addition, the government has raised the tax exemption on dividends remitted from overseas subsidiaries from 95% to 100% starting next year. Until now, dividends brought into Korea from foreign subsidiaries were taxed, despite long-standing criticism of double taxation, since those profits had already been taxed locally.

As a result, companies tended to keep profits overseas rather than remit them. The government now aims to resolve this issue, though it has not clarified whether the measure is temporary. With the outlook for the won extremely bleak and further depreciation of more than 10% expected, would any rational company convert dollars into won just to gain a 5% tax benefit?

In any case, following these measures, the exchange rate—which had been surging toward 1,500 won—plunged to 1,448 won. Ironically, the very measures intended to curb the surge are instead fueling expectations of further depreciation.

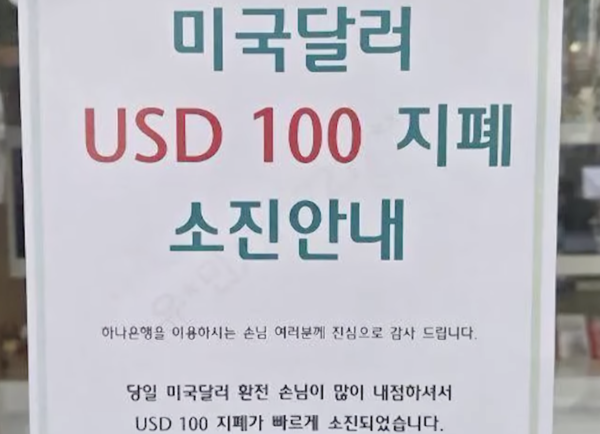

As a result of the measures announced on the 24th, $100 bills disappeared from the market. When the exchange rate fell by nearly 40 won in a single day, people rushed to hoard dollars, seizing the opportunity. A major bank branch in Gangnam even posted a notice stating that all $100 bills had been sold out.

Speculative psychology is activated by exchange-rate volatility. Such hoarding occurs because many people believe the exchange rate will continue to rise.

While the government’s sense of urgency is understandable, few believe that such fragmented and superficial measures can rein in a won exchange rate already on an upward trajectory. Exchange rates are not temporary phenomena; they move in response to a country’s fundamental economic structure.

The fundamental factors directly affecting exchange rates include the following:

The policy interest rate gap between the U.S. and Korea.

Korea’s base rate stands at 2.5%, while the U.S. rate is 4.25%, creating a 1.75 percentage-point gap. Naturally, capital flows toward the higher-yielding U.S. market.

Economic conditions and macroeconomic indicators:

These include growth rates, the current account (trade balance), and inflation. Korea’s growth is stagnating, and exports—excluding semiconductors—are declining. Inflation has risen to 2.4%, exceeding the Bank of Korea’s 2% target, due to large-scale distribution of relief funds. Inflation is expected to rise further due to exchange-rate effects.

Domestic political and psychological factors:

Domestic politics remain unstable, and under U.S.–Korea tariff negotiations, Korea is expected to invest a total of $350 billion in the U.S., including $20 billion annually. In addition, the construction of U.S. factories by major conglomerates will generate massive future dollar demand.

A decline in foreign direct investment:

Korea’s unfavorable investment climate for foreign companies is widely known. With one of the world’s strongest labor unions, the Yellow Envelope Act, and revisions to the Commercial Act, even existing foreign firms are finding it difficult to operate. There is little incentive for new investment, sharply reducing demand for the won.

Only rising dollar demand is anticipated. The balance between dollar supply and demand versus won demand has collapsed. With Korea’s economic fundamentals unstable, investors avoid holding won and prefer dollars.

These are issues the government must address through medium- to long-term structural reforms, not through short-term and superficial measures such as capital gains tax exemptions or pension fund hedging.

Hasty, temporary measures aimed at extinguishing an immediate fire only amplify investor anxiety and reinforce expectations of future exchange-rate increases, worsening the situation.

Using the National Pension Service as a tool for currency defense is particularly dangerous. To the author’s knowledge, no advanced economy has ever mobilized its national pension fund for exchange-rate defense at the government’s request.

If the exchange rate continues to rise, the NPS alone cannot defend it—and the losses it would incur are obvious. Who will be held responsible for those losses?

It is puzzling that the media and the opposition remain quiet. Mobilizing the national pension for currency defense is extremely risky and directly affects the public interest.

Instead of exploiting special prosecutors for political gain, both ruling and opposition parties should launch a special investigation into the government agencies responsible for allowing the exchange rate to deteriorate to the point where even the pension fund is being deployed.

Are special investigations into Yoon Suk-yeol, Kim Keon-hee, or the Unification Church really that important? Frankly, the public is fatigued by news related to Yoon Suk-yeol. Such investigations may matter to politicians, but they have little impact on the daily lives of ordinary citizens.

The exchange rate is different. We can see our paychecks shrinking day by day. As prices rise and real income falls, the lives of ordinary people grow increasingly difficult.

We must urgently identify what went wrong in the process that led to this exchange-rate surge, determine responsibility, and hold those accountable. Fundamental solutions require rebuilding the system with new leadership. The current financial authorities have already failed in economic policymaking and must take responsibility.

In corporations, executives or division heads who fail are held accountable and step down. Only then can new people with fresh perspectives propose solutions.

Now that the government has directly intervened in exchange-rate defense, the risk of being designated a currency manipulator by the U.S. Treasury looms. Just three months ago, in October, Korean and U.S. financial authorities issued a joint statement prohibiting currency manipulation for unfair competitive advantage. Yet the government has now engaged in direct intervention.

As is well known, designation as a currency manipulator carries severe disadvantages. Unable to move forward or backward, Korea’s economy appears to be entering a vicious cycle. The outlook for the Korean economy is bleak and difficult to predict.

With the inauguration of the Lee Jae-myung administration, the initial missteps—purging the previous administration and distributing massive amounts of relief funds—set the wrong course from the start. When the first button is fastened incorrectly, everything that follows goes awry, leading only to repeated policy blunders.

#CurrencyCrisis #ExchangeRateParadox #EconomicFundamentals